CO2 capture: will technology save us?

Climate change is likely the most critical problem of our era, and we have now reached a critical juncture. The consequences of climate change are unprecedented and range from changed weather patterns that threaten food production to rising sea levels that increase the risk of devastating floods.

If we do not take action immediately, it will become more challenging and more expensive to adjust to these impacts in the future.

An economic interest

From an economic standpoint, we can employ mitigation strategies, which minimize or limit the emission of greenhouse gases (GHGs) into the atmosphere, thus reducing the intensity of the impacts of climate change. The Intergovernmental Panel on Climate Change (IPCC) has emphasized that in order to meet the objectives of the Paris Agreement and limit the temperature increase to 1.5°C, we must adopt technologies that remove carbon from the atmosphere, in addition to increasing our efforts to lower emissions. Carbon Capture and Storage (CCS) is one such technology that could play a vital role in combating global warming.

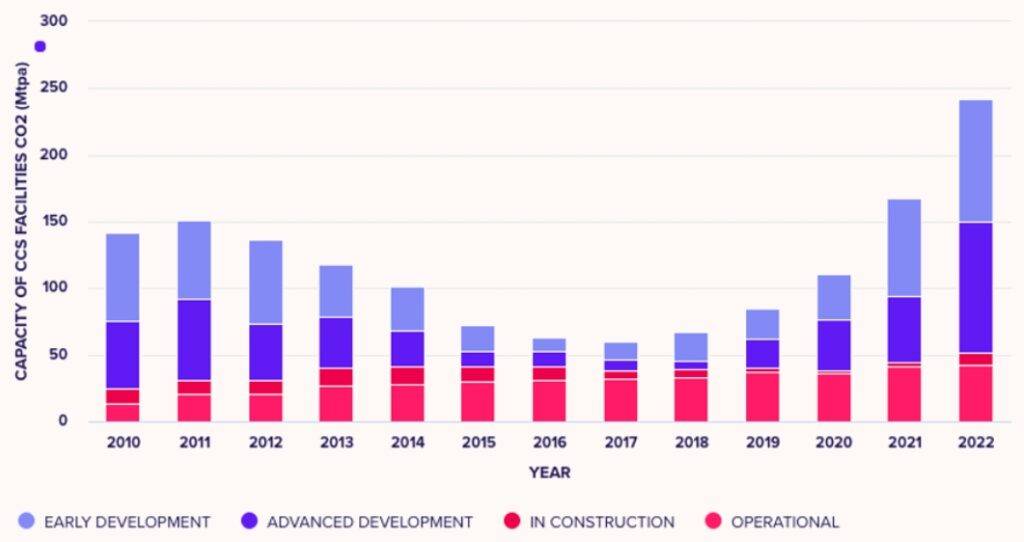

“The number of installations has increased by 44% since 2021”.

As attendees of COP27, we had the opportunity to engage in discussions with various government representatives and international organizations, as well as interact with experts from the industry. The highlight of our experience was that the technology that received the most attention was Carbon Capture and Storage (CCS).

The shift from aspirations to actual implementation is unmistakable, as evidenced by the investment data in CCS. In 2022, the total capacity of CCS projects under development was 244 million tons per year of carbon dioxide. But how does it actually work?

CCS explained

In essence, CCS involves capturing carbon dioxide emitted from power plants or industrial processes like steel or cement production, transporting it, and then safely storing it underground. Saline aquifers or depleted oil and gas reservoirs, which are typically located more than 1 km below the surface, are potential sites for carbon storage. Another related concept is CCUS, or Carbon Capture, Utilization, and Storage, which aims to recycle carbon in industrial processes by converting it into products such as plastics, concrete, or biofuels instead of just storing it.

As of September 2022, the Global CCS Institute reports a total of 196 CCS projects, with 30 of them already in operation and 153 still in development. The number of CCS installation projects has increased by 44% since 2021, continuing the upward trend in the number of CCS projects being constructed that started in 2017. Over the past two decades, experience has shown the versatility of CCS and its critical role in managing emissions from industrial processes.

We anticipate a growth in strategic partnerships and collaboration through CCS networks to drive implementation. With several blue hydrogen projects being developed globally, clean hydrogen and other low-carbon fuels are also contributing to the growth of CCS. Direct air capture with CCS, also known as Direct Air Capture with Carbon Storage (DACCS), has also gained significant attention and investment this year, with billions of dollars being allocated towards scaling up this technology.

Solution for the ecological transition, at the expense of reducing emissions?

While these technologies hold promise, they remain controversial for both financial and political reasons. The cost of developing these strategies is significant and the results, while promising, are still uncertain. Additionally, a focus on carbon sequestration technologies could divert attention away from the crucial task of reducing emissions. Some detractors argue that policies promoting the deployment of CCS serve as “enablers of climate inaction.”

“The implementation of CCS requires the involvement of government authorities, making it a highly political issue.”

CCS requires significant investment, which can be a barrier for attracting investors, especially since the returns may not always be guaranteed. For example, in the United States, the Department of Energy initiated 11 CCS projects at the end of the 2000s, including 8 in the coal sector, at a cost of 684 million dollars. Out of these 8 projects, only one was completed and operated from 2017 to 2020. In Europe, CCS projects are also increasing, with Northern European countries (Norway, the Netherlands, and the United Kingdom) announcing plans to invest more than

CCS requires significant investment, which can be a barrier for attracting investors, especially since the returns may not always be guaranteed. For example, in the United States, the Department of Energy initiated 11 CCS projects at the end of the 2000s, including 8 in the coal sector, at a cost of 684 million dollars. Out of these 8 projects, only one was completed and operated from 2017 to 2020. In Europe, CCS projects are also increasing, with Northern European countries (Norway, the Netherlands, and the United Kingdom) announcing plans to invest more than €5 billion in CCS.

According to a report from Ifri, the cost of capturing, transporting, and storing CO2 ranges from 40 to 200 euros per tonne with currently available technologies, with the higher range corresponding to particularly polluting infrastructures like power plants and waste incineration facilities. Despite the decreasing cost of the technology, this cost still remains higher than the price of CO2 on the carbon market, undermining the incentives for private actors to invest in CCS.

Therefore, the deployment of CCS is highly dependent on the actions of the public authorities, making it a highly political issue. The question of public investment in CCS reflects a country or region’s strategy for achieving the 1.5°C target set by the Paris Agreement, and their vision for an ecological transition. Currently, the leaders in CCS are states and actors whose economies rely on fossil fuels. For example, in Europe, CCS is mainly promoted by the political leaders of countries whose energy mix is primarily based on oil and gas.

In the world, the leading states in terms of these technologies are Canada and the United States, which also have a highly concentrated energy mix centered around fossil fuels. During the COP27 negotiations, Gulf states, particularly the United Arab Emirates, expressed their enthusiasm for CCS and presented it as one of their primary means of achieving net zero emissions by 2030.

At COP27, the presence of oil and gas producers was significantly higher, with 25% more companies compared to the previous COP in Glasgow. These companies, such as ExxonMobil and Big Oil in the United States, TotalEnergies and Technip in France, were among the main supporters of CCS development. Some people speculate that these companies are investing in CCS as a way to divert public attention from their oil and gas operations, in order to preserve them. CCS was at the center of their discussions about decarbonizing their activities.

On the way to COP28

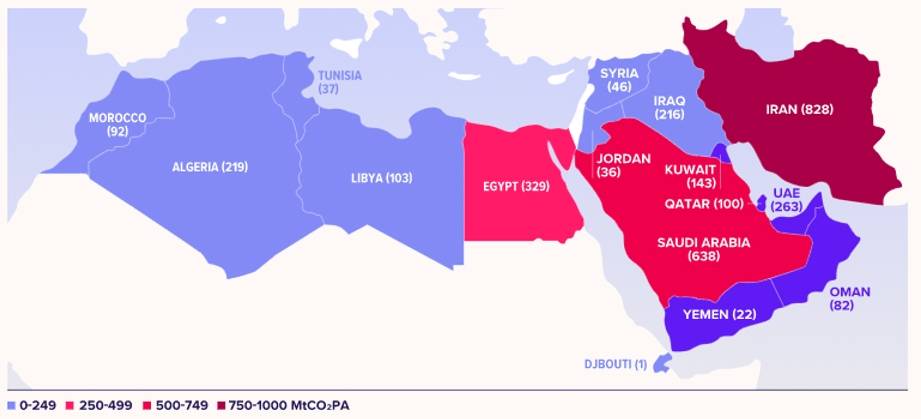

The Middle East and North Africa (MENA) region is considered one of the most intensive in terms of greenhouse gas emissions, with countries like Qatar, Kuwait, United Arab Emirates (UAE), Bahrain, and Saudi Arabia among the top ten highest carbon emitters per capita.

In Sharm, discussions about the reliance on technology mainly center around Carbon Capture and Storage (CCS). Interestingly, one of the leading global advocates for this technology is the United Arab Emirates, which will host the Conference of the Parties in 2023.

A promising technology, CCS always takes center stage in international discussions on climate issues, and its development should be a part of a comprehensive transition strategy with specific and tangible goals.